Originally published in Today's Farmer

Current Market Conditions

Harvest is complete on nearly half of US corn and soybeans acreage, and with each passing week more confidence can be portrayed regarding 2023 production for the world's largest and second largest producing country of corn and soybeans, respectively. The 2023 US crops have not held up to lofty pre-season expectations and it is likely both will record below trend yields for the second consecutive year. The United States Department of Agriculture lowered both national corn and soybean yields 0.8 and 0.5 bushels/acre, respectively, in the October Production Report. There is a marketing saying that small crops tend to get smaller as the season progresses. Historically, this statement has held up under observation. Over the past three decades, corn yields have declined ten times in October then declined again in November nine times. During that same span, soybean yields declined thirteen times in October then again nine times in November. The relatively tight supplies of soybeans and the decline in US soybean production in October suggests the soybean balance sheet is vulnerable, especially if the US crop declines further or weather challenges threaten the infant Brazilian crop. The market's attention will shift from US production to South American production by Thanksgiving. This article covers the prospects for soybean production, demand, and prices in the months ahead.

2024 Soybean Outlook

Between August 29 and October 12, a period of 32 trading days, the nearby futures contract for soybeans declined $1.41/bushel as reports of surprisingly better yields and uninspiring demand convinced traders lower prices would be required to balance supply and demand. This bearish sentiment was reinforced on September 29th when the Grain Stocks Report indicated US soybean stocks on September 1st, the official start to the 2023/24 soybean marketing year, were higher than expected by about eleven percent- increasing available supply. On the demand side, export commitments by international buyers of US soybeans through September were 38% lower than the average for the same period over the previous three years and soybean crush in August was a disappointment relative to expectations. It seems there was justification for lower prices as harvest begun. Additionally, ample soybean supplies globally have kept US soybeans priced above competitor prices on the international market. However, optimism might be growing as the calendar flips to November, and it is coming in a variety of ways.

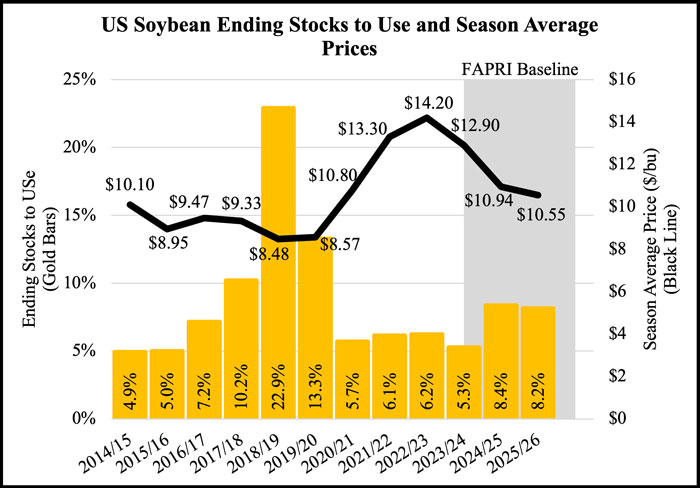

- US supply remains tight heading in 2024 due to reduced harvested area, flat yield, and lower beginning stocks. The expected 2023/24 ending stocks to use ratio of 5.3% is down from 6.2% in 2022/23. The Food and Agricultural Policy Research Institute (FAPRI) at the University of Missouri anticipates the stocks to use ratio rebounds in 2024/25 on stronger US production.

- China, the world's largest buyer of soybeans, also is facing tightening supplies. While drought reduced soybean production in the US, heavy rains and flooding reduced Chinese soybean production. At the same time Chinese feed demand also seems to be returning. After negative margins and relatively high input prices for feed constrained China's swine sector's inclusion of soybean meal early last year, soybean meal inclusion rates in feed production have returned to historical levels. China's soybean imports from the world for the year ahead are forecasted just slightly under the record set last year. China's commitments of US soybeans are still behind the seasonal average, but sales picked up in October.

- Continued growth in domestic use of soybean oil and domestic soybean crush. US biomass-based diesel production capacity continues to grow. In two years, capacity has increased 68%. Almost all the growth coming from rapid growth in renewable diesel production to serve domestic markets. FAPRI expects domestic soybean crush to increase 90 million bushels this year over last year and continue to increase the next five years. This assumes no federal or state policy changes as FAPRI considers only current policy. The rate of expansion could be quicker if states considering policy changes do in fact pass legislation to create or expand renewable fuel programs.

Final Thoughts

US soybean prices have declined from prices experienced earlier in the year. Price in mid-October traded $1 per bushel lower than the crop insurance base price set in February. US soybean production in 2023 was down from original expectations on reduced acreage and lower yields. South America soybean production will draw most of the market attention in the weeks and months ahead where weather will get the last say, but there is a growing sense that the harvest lows may have been found in early October and that prices might finish the calendar year on an upswing. However, the party might not last too long as larger acreage, stronger yields and higher global production appear to be burdensome in 2024.

Author calculations using production data from USDA.