Originally published in Today's Farmer

Current Market Conditions

Yield variability exists every year to some degree, but 2023 stands out as uniquely variable because it was not limited state to state or county to county, but one end to the other end within the same field. Periods of dryness and crippling heat across the United States required timely rains to encourage crop development. Areas receiving timely rains have average to even above average crop yields while other areas are left wondering "what if". Highlighting this great degree of yield variation across the country was the National Agricultural Statistics Service (NASS) September Crop Production Report indicating Ohio corn yield a record 195 bushels per acre. While not a record, Iowa's 2023 corn yield is estimated at an impressive 200 bushels per acre. For large portions of Missouri, the beneficial timely rains never came. At 145 bushels per acre and a 9.9% year over year decline in yield, Missouri trails only Virginia at 10.2% in 2023. The big asterisk to add to the previous sentence- Virginia had a record corn yield in 2022 while Missouri struggled with the first of two consecutive years of drought. Nationally and globally, corn is not scarce. However, for a state like Missouri where a sizable portion of the corn grown is used for feed, there will be areas with relatively high basis levels to encourage supply. The outlook for corn markets into 2024 presents a few interesting coffee shop discussion topics and some long run concerns. While yield potential has been the headline market mover since June, the focus will soon quickly shift to corn demand, which has been uninspiring to date.

2024 Corn Outlook

If the 2024 corn outlook for production, demand, and prices was a book, the chapters would be rich with drama. Starting with production, how likely are producers to plant an expensive corn crop when input costs remain stubbornly high and prices for December 2024 continue to decline? This same question was pondered in early 2023 just before US producers responded by planting 95 million acres- the most corn acres during the decade. The roughly 6.3 million additional planted acres in 2023 relatively to 2022 is part of the reason corn prices have not moved higher on lower yield revisions. Early estimations for 2024 cost of production suggest a 6-8 percent decline in total costs for Missouri producers. The other reason corn prices have not moved higher on yield declines is due to corn demand that struggled to gained traction. At every opportunity to be optimistic there was a new hurdle facing US corn producers. A couple examples:

- Almost a year ago, low Mississippi River levels limited barge traffic and increased transportation cost per bushel.

- Railroad worker strikes and the lack of ability to move ethanol stopped ethanol production and corn grind.

- About the time US corn exports were becoming competitive, Brazil produced a record corn crop and quickly filled many international markets.

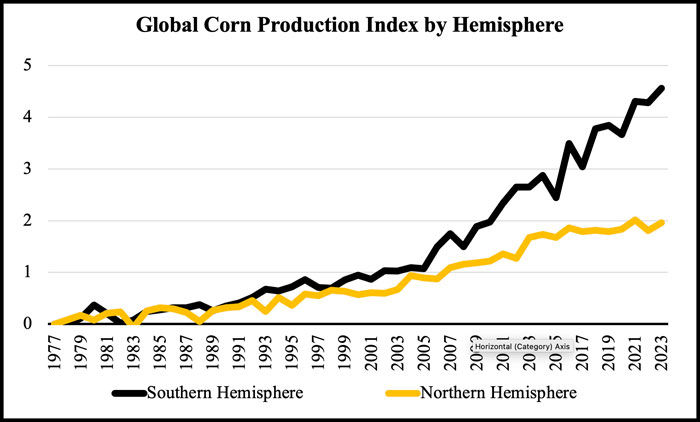

Fast forward a year, US in-land water channels are again a concern with water levels approaching record lows set last year and US export prices remain uncompetitive with major exporters including Brazil. Outside increasing South America production competition there are three other international questions related to the corn market that offer opportunities to debate. First, does the war in Ukraine continue to intensify and threaten international feed grain supplies? Ukraine represented close to 13% of exportable supplies of feed grains prior to war. Second, is this the year China once again imports relatively large quantities of corn and a high percentage from the US. In the past decade, market analysts frequently overestimated eventual Chinese corn imports and underestimated soybean imports. In November 20222, the Chinese government expanded biotech approval to additional Brazilian export companies, which then kicked off the rapid expansion in Brazilian corn production and eventual exports to China this past spring. At this point, it seems unlikely that Chinese imports of US corn will reach the volumes experienced in 2021/22 when large Chinese purchases of corn, sorghum, distillers grains, and ethanol increased US prices. The final debatable point, does Mexico implement their ban of non-GMO corn? Mexico is routinely the top annual buyer of US corn, representing around 30% of US corn exports. Conversely, the US is the primary supplier of corn to Mexico representing 90% of Mexico's annual imports. These rates would suggest that it would take 650 million bushels of non-gmo corn or four million acres to completely substitute the amount of corn the US annually sells to Mexico. Of all the market movers listed above, it is the growth in Southern hemisphere corn production that could present the highest likelihood of influencing prices and production in the US over the next couple years. Southern hemisphere production has rapidly expanded and has further room to grow over the next decade.

Final Thought

There are multiple stories worthy of debate at the local coffee shop regarding the outlook for 2024 US corn prices. While a surge in Chinese corn import demand and a reduction of available Ukrainian feed grain production would support corn prices, low Mississippi water levels, continued growth in Southern Hemisphere corn production and a gmo corn ban by Mexico would further erode prices. The world currently has enough corn to supply end users and the season average price for 2023/24 is estimated to be $4.95 per bushel- close to cash bids in Missouri Mid-September.