Originally published in Today's Farmer

Current Market Conditions

Just a few 2023 corn acres remain standing in the United States as the calendar flips to December. As a reminder, corn still standing is considered on farm storage in the quarterly Grain Stocks Report published by the United States Department of Agriculture (USDA). It is typical for The Upper Great Plains states to have some standing corn left to harvest at the end of the year.

With harvest nearly wrapped up across the United States, the supply side of domestic grain and oilseed balance sheets can be calculated with some reasonable certainty with one exception- final harvested acreage. The National Agricultural Statistics Service (NASS) uses Farm Service Agency (FSA) farmer reported planted acreage number starting in August to estimate total planted acreage but does not account for historical deviations between harvested and planted acreage until January. The difference between planted and harvested acres is commonly referred to as failed acreage. However, the term failed acreage is a little misleading as corn and grain sorghum chopped for silage would be included in the "failed acreage" total. A larger than average failed acreage number is possible in 2023 for multiple crops. For corn and grain sorghum, poorly pollinated drought impacted fields were likely chopped for livestock feed to help offset dry pastures and lower than normal hay production. For late planted and double cropped soybeans, the bean pods never filled, and many fields were terminated to jump start winter wheat seeding. Large quantities of failed acreage have historically meant two things- lower total harvested acres and higher national average yields. The first observation is rather straight forward and would be bullish to commodity markets. The second observation uses the assumption that failed acres are the lowest yielding fields, meaning the yield average increases when removed. Alone, an increase in the national average yield is bearish. Therefore, the magnitude of each of these two observations is important.

With any revisions to harvested acreage and domestic supply coming in January, at the earliest, commodity markets have turned attention away from domestic production and turned toward demand prospects. Previous articles covered outlooks for corn and soybean use for biofuel production. This article provides an update on US grain and oilseed exports for the 2023/24 marketing year.

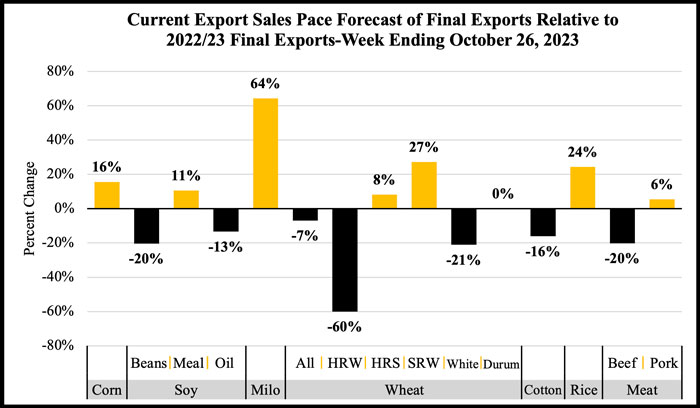

2023/24 US Gain and Oilseed Export Update

International exports of US grains and oilseeds are a non-trivial portion of demand for US producers. Exports on average account for 15%, 57%, 47%, and 47% of US corn, grain sorghum, soybeans, and wheat production, respectively. The US share of global exports has declined for each crop over time as domestic uses like biofuels have limited exportable supplies and growth in international production has increased competition for US commodities in the global marketplace. However, surprises in export volumes can rattle markets and are therefore still relevant. The chart below illustrates how the export market for 2023 is fairing compared to 2022. A couple general observations across all crops.

- The US dollar index, which compares the buying power of the US dollar to other currencies around the globe has remained elevated making US commodities more expensive to buyers relative to commodities from other major exporting countries.

- Similar, exportable supplies in international countries impact the demand for US products on the global marketplace. Large quantities of exportable Russian wheat and South American corn and soybeans in 2023 has reduced the demand for US commodities in the short run.

- Domestically available exportable supplies are dependent on production and domestic uses. Decreases in US production or increases in domestic use limit exportable supplies. The US has had multiple years of below trend production after a stretch of above trend production.

A couple comments about specific commodities through October

Corn

Total corn export commitments are reported at 719 million bushels, roughly 60 million bushels behind the pace needed to hit the export estimate for 2023/24 of 2,025 million bushels. However, the pace would suggest 2023/24 exports will exceed corn exports from 2022 by 16 percent. Amidst the talk of banning genetically modified corn, Mexico has consistently led weekly sales volumes and represents 52% of total committed 2023 US corn.

Milo

It has been a strong year for US milo exports with total commitments to date for the 2023/24 marketing year at 115 million bushels- 57 million bushels above the pace needed to hit the current export target. If the pace is maintained, US grain sorghum exports will exceed last years exports by 64%. Nearly all of the current export commitments are held by China or unknown destinations also assumed to be China.

Soybeans

Commitments of US soybeans of 959 million bushels are 109 million bushels below the seasonal pace needed to hit the current export forecast of 1,755 million bushels, which is 12% lower than the agencies 2022/23 estimate. If maintained, US soybean could fall year over year by 20%. Brazil continues to maintain a market share of roughly 30 to 40 percent of soybeans going into China each month. These are historically high monthly volumes for Brazil and explain why US soybean exports are below expectations. What has been most discouraging for US soybean exports is the decline in sales for December and January delivery. The decline in sales relative to previous years for the prime export sales window represents a bearish concern to prices.

Soybean meal

Export commitments of soybean meal are nearly 1 million short tons above the season average pace needed to hit the 2023/24 export forecast. What is also promising is the broad distribution of countries holding US soybean meal commitments. It is possible the US will be able to continue exporting soybean meal at relatively high quantities through February. At which time Argentina will have soybeans to crush.

Wheats

Total commitments of US wheats at roughly 416 million bushels are slightly above the pace needed to hit the current 2023/24 export projection of 700 million bushels. Across the five major classes of wheats- exports of Hard Red Spring and Soft Red Winter wheats are exceeding the pace needed while Hard Red Winter, White and Durum wheats lag their seasonal pace. Export declines for Soft Red Winter wheat compared to recent averages is particularly noticeable considering the large quantity of Soft Red Winter wheat the US has in exportable supplies. Lack of export sales is one reason Soft Red Winter wheat prices have declined from harvest.

In summary, export sales this time of year usually pick up as international buyers take advantage of harvest lows. While sales of US grain and oilseeds have increased from level experienced in August, they are seasonally low. There are three exceptions to the previous statement: 1. US corn sales to Mexico for both 2023/24 and 2024/25; 2. US grain sorghum sales to China; and 3. US soybean meal sales as the US takes advantage of a significantly reduced crop in Argentina last year.

Author calculations using production data from USDA.