Originally published in Today's Farmer

Current Market Conditions

Grain and oilseed markets moved lower to end 2023 and start 2024 as concerns over South America's crops deteriorated and spurts of international demand remained rather mute. The trend is expected to continue until more is know about Brazilian corn potential and 2024 US acreage expectations are released March 29, 2024.

In early January, much attention continued to be given to El Nino's impact on South American production. Digging into the numbers suggested it was going to take either a larger reduction in production relative to expectations or lower prices to clear the market. Lower clearing prices eventually won out. There are local cash markets that will need product periodically and will have to bid up basis prices to attract farmer selling as it does not appear evident futures markets will do that work over the next couple months. At least not for soybeans. While odds are growing Brazil will not produce a record soybean crop, Argentina is expected to increase their production 20 million metric tons year over year- more than enough to make up the difference. The world has the needed soybean supplies and without additional bullish news, the futures market's path of least resistance is lower.

Conversely, corn's price potential is more uncertain. Seventy-five percent of Brazil's corn crop is planted after soybeans. Late planted corn accompanied with an early frost or dry weather would shrink Brazil's corn output and rally prices. In 2015, EL Nino delayed corn planting and shrunk Brazil's corn output relative to expectations 25%. A similar adjustment relative to expectations in 2024 (roughly 1.2 billion bushels) would be enough to change market psychology and move prices higher. It is still early in the season for Brazil's second crop corn and expectations are the crop only marginally decreases. Corn markets continue to find strength on near record corn ethanol grind and supportive export volumes.

Outlook for 2024 Expenses and Returns

In the United States, whispers can be heard regarding 2024 total acreage and crop mix. Unexpected acreage shifts across crops can change crop market fundamentals quickly. Relative crop returns for the year ahead across crops are only one factor influencing planted acres across the US. The relationship between crop insurance guarantees is another factor and a warm dry spring has historically indicated higher than expected corn acres.

Nationally, expected returns and average weather indicate a combined corn and soybean acreage value of 178.4 million acres- down marginally from 178.5 million acres in 2023. Note- there was a four-million-acre shift from soybeans to corn relative to expectations last year largely due to warm weather at planting and improved profitability potential. The shift caused a rally in soybean prices. Corn acreage is expected to fall from 94.9 million acres to 90.7, while soybean acreage increases from 83.6 to 87.7 million. The closely watched new crop soybean to corn ratio fell in December on lower soybean prices relative to corn. At 2.44:1, the soybean to corn ratio would suggest new crop prices favor neither corn nor soybeans. The ratio favored corn acreage expansion this time last year, which was realized at planting.

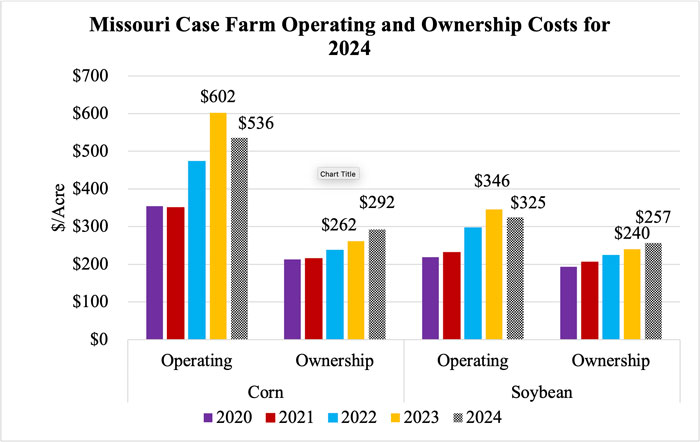

As mentioned above, expected profitability between corn and soybeans can also influence acreage shifts. Every farm has its own cost structure, and it is recommended to calculate enterprise budgets annually. The University of Missouri publishes a series of 30 crop and livestock enterprise budgets every year producers can use to help plan for the year ahead. Using a west central Missouri case farm, total costs for corn and soybeans are expected to decline roughly 4% in 2024 relative to 2023. However, not all costs are expected to decline in 2024. While operating expenses that include seed, crop protection, and fertilizer are expected to be lower in 2024, ownership costs such as land rent, machinery, labor, and interest expense are all expected higher year over year. The graphic below illustrates operating and ownership costs for corn and soybeans relative to previous years.

Returns over total economic costs for the west central Missouri case farm suggest losses of nearly $30 per acre for corn and gains of $44 per acre for soybeans in 2024. Relative crop returns will vary across the country. However, these returns support a gradual shift to soybean acres from corn in 2024. Is it a full four-million-acre shift? That is the question that will be answered over the next two months. Outside a shift in market phycology, soybean futures prices will continue to drift lower to balance supply and demand. New crop corn prices are little more uncertain at the present time.

Author calculations using production data from USDA.