Originally published in Today's Farmer

Current Market Conditions

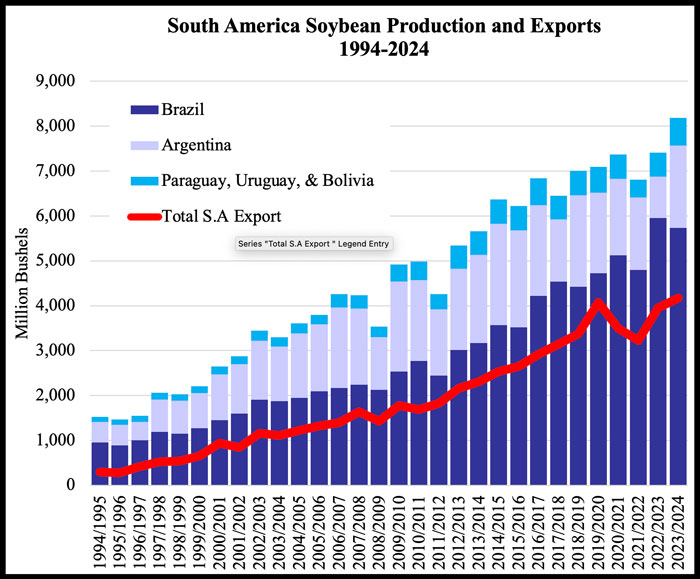

Fundamentally, there is little in the grain and oilseed complex to spark a price rally for old crop supplies. Global supplies are plentiful, with a high portion unpriced. Yes, Brazilian corn and soybean production estimates have decreased the last couple months by 200 and 276 million bushels, respectively, and the final volumes could still be lower. Conversely, Argentina corn and soybean production is estimated to increase nearly 800 and 920 million bushels year over year, respectively. The rebound in Argentia production after two years of intense heat and drought is a contributing factor why old crop markets seem undeterred by declining production estimates in Brazil (see image). Market moves lower continue to be the path of least resistance in the search for supply and demand equilibrium. This article looks to provide commentary on if it is time to sell old crop supplies.

A couple signs that point to a near-term bottom for old crop corn:

- Corn demand is increasing with declining prices. The familiar adage "The cure for low prices is low prices" still applies. Corn used for ethanol production has become one of the solid domestic use factors in 2024, with corn and ethanol prices at levels positive enough to sustain output. Corn used for ethanol production is up 97 million bushels or 4% from the same period last year. Continued strength in corn used for ethanol demand is expected. International demand for US corn picked up in February on lower prices. Total export commitments of 2023/24 corn of 1,425.7 million bushels is 371 million bushels ahead of the level experience at the same time last year. Export sales in February averaged 30% higher than the weekly volumes in January.

- Commodities are used as a hedge against inflation in investment portfolios. Global traders tend to build ownership of futures and options positions of commodities when the sector believes inflation rates will be rising. Conversely, speculative investors tend to sell positions when they believe inflation is cooling. For data provided February 6, 2024, managed money traders held near record short positions of Chicago corn, soybean and wheat future and option contracts. This trend started to develop as the Federal Reserve's Open Market Committee started increasing the benchmark for short-term interest rates bringing down inflation. The preferred measure of inflation has not reached the Committee's target of 2% and came in above expectations in the most recent update. Uncertainty over inflation expectations, as we are experiencing now, could encourage investors to buy back into the market to collect their position profit and protect against increasing inflation. Such a move would be supportive to commodity markets.

A couple signs that suggest soybean prices may still move lower:

- Domestic soybean crush has been strong but might currently be outpacing demand. Investment in renewable diesel production and one of its feed stocks, soybean oil, has been a boom to soybean demand in 2023/24. Since the marketing year started in September, soybean crush volumes have set monthly soybean crush records every month. Soybeans crushed exceed the seasonal pace needed to hit the current target by 25 million bushels. However, soybean oil stocks have increased relative to expectations three consecutive months. With a lower-than-expected soybean crush number and a larger than expected soybean oil stocks volume- implied soybean oil demand in January was the lowest monthly volume since last April. The build out of renewable diesel and soybean oil demand will continue to be choppy. At this moment- supply of soybean oil is slightly exceeding demand and a bearish tint to the soybean market.

- US soybean exports continue to remain uncompetitive on the global market. Through mid-February, US soybean export commitments of 1,426 million bushels are 320 million bushels lower than at the same point last year. Additional sales are likely to be limited until this summer. Soybean export prices for US soybeans of $467 per metric ton compared to export prices in Argentia and Brazil of $427 and $404 per metric ton, respectively.

To summarize the market outlook for old crop supplies, soybean markets remain under pressure of burdensome supplies and a general softness in demand. Corn prices may be reaching a point where demand and supply are relatively in alignment and could find a small rally. A large rally in corn is difficult to see due to the quantity of unsold old crop supplies around the country. The question then becomes- does a rally in corn price justify the storage costs?

As a reminder, storage costs at a commercial elevator are the storage charges and cost of money, where storage costs on farm include the same cost of money charges along with equipment repair and shrink. The general costs of shrink are roughly $0.08 and $0.11 per bushel for corn and soybeans respectively. Cost of money is equivalent to the opportunity cost of that money if the bushels were sold. At current interest rates and commodity prices, interest expenses on stored grain would be 2.6 and 7.3 cents for corn and soybeans, respectively. Markets would have to rally the sum of the monthly physical storage cost plus cost of money expense to justify storing grain one more month. Neither crop has great odds of covering, but corn appears to have better odds than soybeans.

Author calculations using production data from USDA.