Originally published in Today's Farmer

Current Market Environment

Global corn, soybean and wheat supply expectations have deteriorated since the Planting Intentions Report released by the United States Department of Agriculture in late March. Persistent and consistent rain fall has limited suitable field workdays in portions of the US. Planting progress for corn is behind average and it is likely the share of corn planted late will exceed levels experienced in recent years. Share of late planted corn is an indicator of national average corn yield. The higher the share of late planted corn, the higher the probability the national average corn yield falls below trend. Late planted corn in this analysis is defined as corn planted after May 20. Argentina corn production expectations have also diminished due to disease. Leafhoppers caring the corn stunt disease have impacted roughly 3 million acers and threatened production for the 2023/24 and 2024/25 growing seasons. While total global supplies of corn are forecasted to increase most of the increase in production is within the US and China. Corn supplies relative to use outside the US and China are forecasted to be the tightest since 2002.

For wheat, China has flooded the world with cheap wheat supplies. There are signs that trend is ending. Drought and a late freeze have lowered expectations for Russia's wheat crop and the volume of exportable supplies available to the world. India, the world's second-largest consumer of wheat, reported that their government owned wheat stocks are at a 16 year low after two years of low crops prompted sales to support domestic supplies and reduce consumer prices. The combination of declining production expectations by the world's third largest producer and tight stocks by the world's second largest consumer provides some support to global wheat prices.

South America soybean production expectations have also deteriorated in the last month as heavy rains and regional flooding prohibited soybean harvest in the Brazilian state of Rio Grande do Sul. The loss of soybean production in Brazil's third largest production region is anticipated to down 110 to 184 million bushels due to the worst flooding for the region in 80 years.

While global production estimates for corn, soybeans, and wheat have all decline in the last month, the changing fundamentals to support higher prices have encouraged managed money holders to exist their historically net short positions and buy back into a more neutral position. During the first week of May, management money traders were net buyers across the board. The net buys of 107,783 contracts of Chicago soybeans were an all-time weekly record. The net buy of 115,527 Chicago corn contracts was in the top five all time weekly gains. Increasing fundamentals and profit taking by managed money traders has increased futures prices for corn, soybeans and wheats providing an opportunity for producers to offset price risk at profitable prices.

Early Season Grain Marketing

There are two times to market grain: pre-harvest and post-harvest. In some instances, the two seasons might be referred to as new crop and old crop marketings. Once harvest occurs, the pre-harvest marketing option is no longer available and producers are left with the post-harvest season. In most life scenarios, having two options is better than only one.

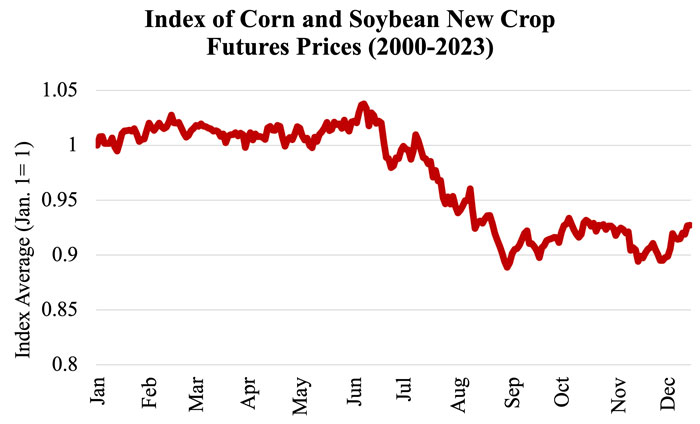

Considering pre-harvest marketing plans can expand the options available to producers. There are two important reasons to consider pre-harvest marketing opportunities: a strong seasonal tendency for grain prices to decline after planting and the opportunity to lock in a price above production costs. Remember, if pre-harvest prices do not reach profitability levels, there is still the post-harvest season. Historical new crop futures price patterns suggest that there are more favorable pricing opportunities in the spring compared to the fall. The graphic below shows an index of new crop corn and soybean prices for the last 24-year crop years; an index of 1 suggests that new crop prices have not changed relative to January. Keep in mind that these are futures prices, not cash prices. After June, new crop futures prices tend to drop anywhere between 8% and 12%. Conversely, new crop basis bids tend to increase in July and August. Managing the two prices separately creates opportunities for producers to increase profitability, and modern crop revenue insurance tools offer producers the ability to price early in the season with confidence. There are many things to consider with marketing plans and not enough space in this article. However, the things to remember are: 1) pre-harvest and post-harvest are the only two seasons to market grain; 2) new crop futures prices tend to decline sharply after planting; and 3) managing futures prices and basis bids separately can be advantageous. The University of Missouri Extension has resources available on grain marketing and marketing plans—reach out to bpbrown@missouri.edu.

Source: Author calculations using date from The CME Group