Originally published in Today's Farmer

The year is 1984 and a young Abner W. Womack, who recognized the value sectorial market and policy analysis provided to agricultural decision makers during the farm crisis of the 1980s, brought his knowledge of commodity markets to the University of Missouri where the Food and Agricultural Policy Research Institute (FAPRI), an organization unlike any other, has existed for forty years. In 2024, FAPRI maintains the same mission to provide reliable, consistent, and objective information on domestic and international market conditions to the public and policymakers. The 2024 U.S. Agricultural Market Outlook Baseline book published in March sets the starting point for analyzing policies and market impacts in the year ahead. This article focuses on FAPRI's short term results for 2024 and 2025.

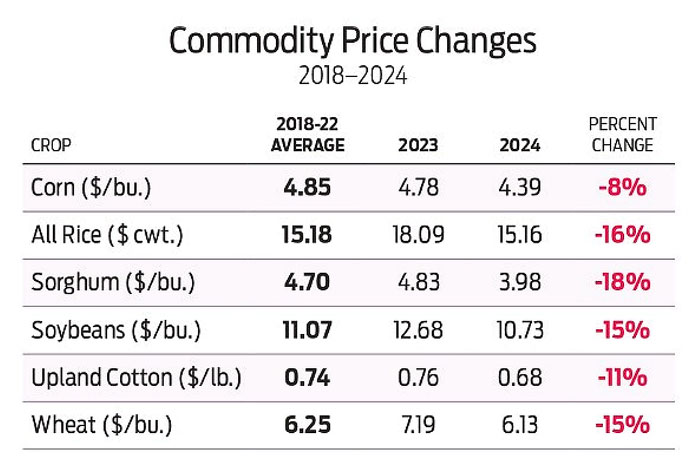

FAPRI's 2024 Outlook for US Commodities

Producers across Missouri are aware by this point prices for grains and oilseeds have fallen from average levels experienced from 2020-2022. The value of the 2023 grain production is also down from initial expectations as a higher share of unhedged grain stored at harvest has been entering the market at lower prices this spring. For 2024 and 2025, the outlook is for lower prices and government payments more than offsetting a slight reduction in production costs. Each commodity is complex with both opportunities and challenges. A general theme across all commodities is growing supplies outpacing demand.

Source: FAPRI-MU

Corn

US corn acreage is expected to decrease 4.5 million acres to 90.1 million acres in 2024 on lower relative profitability. However, the warm dry weather experienced in February is a justifiable reason final corn acreage may end up a little higher. The trend corn national corn yield of 181.4 bushels per acre leads to an expected production of 14,909 million bushels- down from 15,342 in 2023. Corn demand is expected to increase in 277 million bushels with a 386 million bushel increase in exports more than offsetting a 110-million-bushel reduction in domestic demand. The full reduction in domestic demand is contributed to smaller supplies for feed and residual and continued reduction in cattle on feed. The season average price for 2024/24 is expected at $4.39/bushel, down from $4.78 last year. The expectation for 2025/26 is a continued increase in ending stocks and a season average farm price of $4.20.

Soybean

US soybean acreage is expected to increase 4.6 million acres in 2024 relative to 2023 on increased profitability relative to other crops including corn and cotton. The national trend yield is pegged at 52.1 bushels per acre, up from 50.6 bushels per acre in 2023. US supplies of soybeans increases nearly 400 million bushels on the higher acreage and yield forecasts. The higher total supply of soybeans more than offsets a 231 million bushels increase in demand and ending stocks continue to increase from historically low levels. Domestic soybean crush is forecasted to increase 116 million bushels this year to support the growing US renewable diesel industry. The season average prices for 2024/25 of $10.73 per bushel is well below the farm price of $12.68 experienced so far in 2023/24. The price continues to decline in 2025/26 to $10.51 per bushel.

Cotton, Rice, and Wheat

Cotton planted acreage and yield increase slightly in 2024/25. However, harvested acreage is anticipated to return to a normal relationship after two years of drought in the high plains of Texas and other regions decreased the relationship between planted and harvested acres. Cotton prices are expected to decline to 68 cents per pounds down from 76 cents per pound in 2023/24.

Rice planted acreage is expected to drop to 2.66 million acres from 2.89 million in 2023/24 more than enough to offset a small reduction in total use resulting in lower ending stocks. However, the farm price is expected to decline to $15.16 per hundredweight in 2024/25 and then increase to $15.74 per hundredweight in 2025/26.

All US wheat acreage across all classes is expected to decrease 2 million acres to 47.6 million acres in 2024. With nearly flat domestic demand, a 96 million bushel increase in exports represents the entire increase in wheat usage. Ending stocks of US wheat increase to 772 million bushels lowering the US season average farm price to $6.13 per bushel compared to $7.19 per bushel in 2023/24. The all-wheat price falls again in 2025/26 to $5.71 per bushel.

Summary

The outlook for grains and oilseeds suggests a couple years of declining farm income and deteriorating farm working capital. Adverse weather, macroeconomic conditions, or changes in policy could provide opportunities for higher prices, but depending on such developments is not a recommended risk management strategy. Recommended strategies would include having a written marketing plan, detailed enterprise budgets, and firm grasp on whole farm liquidity and solvency ratios.